How to grow a small Forex account

Most retail Forex accounts do not die from one catastrophic trade. They bleed out. The average account holder underestimates how quickly small, repeated losses compound when leverage is applied to undercapitalized positions. Industry disclosures from regulated brokers consistently show that the majority of retail accounts lose money over any given quarter, and small accounts are overrepresented in that figure.

The reason is structural, not psychological — though psychology certainly accelerates the damage. A trader working with $300 cannot absorb the same drawdowns as one working with $30,000, yet many treat the two situations identically. They take the same position sizes relative to perceived opportunity, ignore transaction costs that eat a disproportionate share of a small balance, and overtrade because the absolute dollar gains feel too modest.

There is also the matter of expectation. A new trader who hears that professionals target 10 to 20 percent annual returns will often dismiss those numbers as too slow. So they reach for 10 percent a week instead. The math does not forgive that ambition for long.

Setting realistic expectations for account growth

What does a reasonable growth target actually look like? Professional Forex traders and managed funds generally aim for annual returns in the range of 10 to 25 percent, and even that is considered strong performance over multiple years. Hedge fund data published through major financial outlets confirms that consistent double-digit annual returns place a manager in the upper tier of the industry.

For a retail trader with a small account, the figure may be slightly higher in percentage terms because position sizing is more flexible and capital constraints are less binding. But the difference is not as large as marketing materials suggest. A trader doubling a $500 account in a year is producing a 100 percent return — extraordinary by any institutional standard, and rarely repeatable.

The arithmetic of compounding is where small accounts find their real edge. A 5 percent monthly return, sustained, turns $500 into roughly $898 in twelve months. Sustain it for two years and the figure passes $1,600. The challenge is sustaining it at all. Most traders who hit 5 percent in a strong month give it back within the next two.

Slow growth is not a failure mode. It is the mode.

Choosing the right broker and account type

Broker selection matters more for small accounts than for large ones, and for reasons that are not always obvious. Spreads, commissions, and minimum lot sizes determine whether a trading strategy is even viable at low capital levels. A two-pip spread on EUR/USD costs the same dollar amount whether the account holds $500 or $50,000 — but it represents a far larger percentage of the smaller balance.

Regulation should be the first filter. Brokers authorized by the FCA in the United Kingdom, ASIC in Australia, CySEC in Europe, or the NFA and CFTC in the United States operate under capital requirements and segregation rules that offshore competitors typically do not. The protection is not absolute, but it is meaningful.

Account type is the second decision. Micro and cent accounts allow position sizes as small as 0.01 lots, which translates to roughly $0.10 per pip on most major pairs. Standard accounts requiring 1.0 lot minimums force a small trader into risk levels that no sensible position-sizing model would permit.

Leverage caps differ by jurisdiction. European retail traders are limited to 30:1 on majors, while some other regions allow 500:1 or higher.

Position sizing and risk management on a limited balance

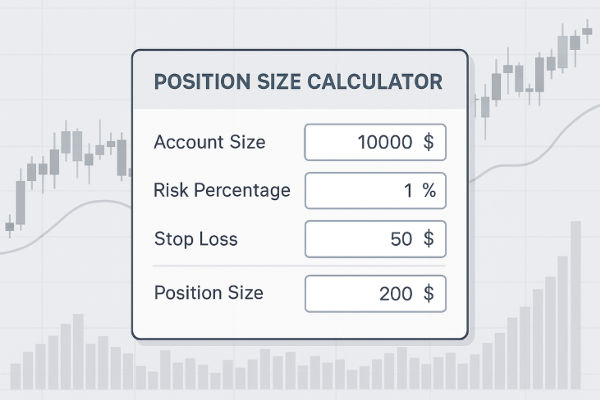

The standard advice — risk no more than 1 to 2 percent of account equity per trade — is often misunderstood at the small-account level. On a $500 balance, 1 percent risk is $5. That is not enough margin for many strategies to work mechanically, because stop losses placed at technically meaningful levels often imply pip distances that, combined with minimum lot sizes, exceed the dollar risk allowance.

Here is where the math becomes unforgiving. A trader using a 0.01 lot position on EUR/USD risks approximately $0.10 per pip. A 50-pip stop loss therefore risks $5 — exactly 1 percent of a $500 account. Widen the stop to 100 pips, and the risk doubles to 2 percent. Tighten it to 20 pips, and the trader is risking only 0.4 percent, which is too little to make the trade worthwhile relative to spread costs.

Position sizing on a small account is therefore a constant negotiation between strategy logic, stop placement, and the smallest tradeable unit. Most beginners resolve this by quietly raising risk per trade. That is the path to depletion, not growth.

Selecting a trading strategy suited to small capital

Not every strategy scales down. Scalping, for example, requires tight spreads and fast execution to extract small price movements profitably. On a small account paying retail spreads, the cost-to-reward ratio rarely works. A scalper targeting 5 pips of profit on a 2-pip spread is giving up 40 percent of the potential gain before the trade even moves.

Swing trading and position trading tend to suit small accounts better. Wider stops mean the spread becomes a smaller fraction of the trade's expected range, and fewer trades per week reduce the cumulative drag of transaction costs. A swing trader holding a position for three to ten days and targeting 100 to 300 pips can absorb a 2-pip spread without meaningful impact on expectancy.

Trend-following systems applied on the daily chart are particularly well suited to capital-constrained traders. They generate fewer signals, demand less screen time, and produce returns that, while modest in absolute terms, compound steadily when risk is controlled.

The strategy should fit the account, not the other way around. Most small-account traders choose backwards.

The role of compounding and withdrawal discipline

Compounding is the mechanism by which small accounts become medium-sized accounts. It is also the mechanism most often abandoned by the traders who would benefit from it most. A 3 percent monthly return reinvested in full grows a $500 account to approximately $713 after twelve months. Withdraw the gains each month, and the account stays at $500 indefinitely.

The temptation to withdraw is strongest when the account is smallest. A $30 monthly profit on a $1,000 balance feels insignificant, so the trader takes it. The next month's $30 is calculated on the same $1,000 base, not on $1,030. Over time, the foregone compounding is substantial — and invisible, because the trader never sees what the account would have become.

There is a counter-discipline worth naming. Withdrawing a fixed percentage of profits, rather than all of them, allows compounding to continue while still rewarding the trader for performance. Some professionals suggest withdrawing 25 to 50 percent of monthly gains and reinvesting the rest.

Whichever approach is chosen, it should be decided in advance. Decisions made in the moment tend to favor consumption.

Tracking performance and adjusting the approach

A trading journal is the single most underused tool among retail traders. Without one, the trader has no reliable record of what actually happened — only an emotional impression of recent trades, which is almost always wrong. Memory tends to amplify the wins and minimize the losses, or the reverse, depending on temperament.

The metrics that matter for a small account are narrower than the analytics packages suggest. Win rate alone is meaningless. A 70 percent win rate paired with an average loss twice the size of the average win produces negative expectancy. The combination to track is win rate, average win, average loss, and the resulting expectancy per trade. Drawdown depth and recovery time complete the picture.

Performance tracking platforms automate much of this when a trading account is linked. They calculate expectancy, profit factor, maximum drawdown, and risk-adjusted return without manual input. The trader who reviews these figures monthly — not daily — gains the perspective needed to distinguish a bad week from a broken strategy.

Adjustments should be evidence-based and infrequent. Strategies need at least 30 to 50 trades before the data carries meaningful weight.

When to scale up and when to step back

Scaling up means increasing position size as the account grows. Done correctly, it is mechanical: position size adjusts proportionally to equity, so a 1 percent risk allocation on a $1,000 balance becomes a 1 percent risk allocation on a $2,000 balance — the dollar amount doubles, the percentage stays constant. Done incorrectly, it means raising risk percentages because confidence has grown faster than capital.

The signal to scale is consistency over time, not a single profitable month. A trader who has produced positive expectancy across at least six months, including at least one drawdown period, has demonstrated something repeatable. Three good months in a rising trend prove very little.

The harder decision is when to step back. Persistent drawdowns beyond the historical norm of a strategy — say, a 20 percent loss when the worst prior drawdown was 10 percent — indicate that something has changed. Either the market regime has shifted, or the trader is no longer executing the system as designed. Reducing position size or pausing entirely is the correct response. Both options preserve capital. Continuing to trade through the drawdown rarely does.