Impact of interest rates on Forex

Capital follows yield. That single behavioural fact explains why a single sentence from a central bank governor can swing the euro a full percent against the dollar within minutes, and why traders who ignore the rate calendar tend to be the ones blindsided by sudden trend reversals.

Currencies are priced relative to each other, and one of the strongest forces shaping that pricing is the return offered on holding a given currency. When a country's interest rates rise, assets denominated in that currency — government bonds in particular — become more attractive to global investors. To buy them, investors must first buy the currency. Demand goes up. The currency strengthens.

The reverse holds when rates fall, or when markets begin pricing in cuts before they actually arrive. This last point is often misunderstood. Forex markets do not wait for the announcement. They move on expectation, on hints, sometimes on a single phrase buried in meeting minutes.

How Central Banks set interest rates

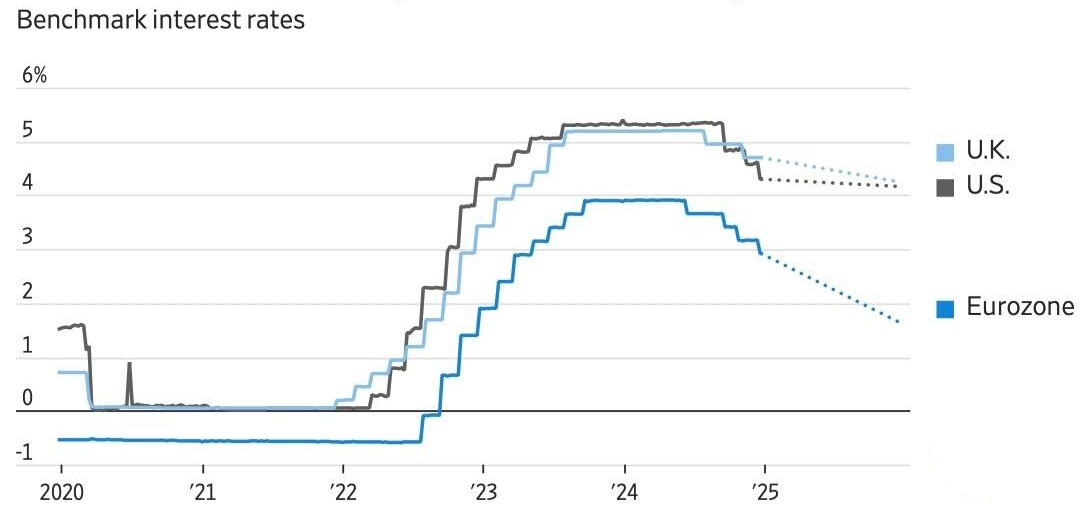

Each major economy has a central bank tasked with setting a benchmark rate — the Federal Reserve in the United States, the European Central Bank in the eurozone, the Bank of Japan in Japan, and so on. These rates are not chosen arbitrarily. They are policy tools, adjusted to manage inflation, employment, and broader financial stability.

The Federal Reserve targets a federal funds rate range. The ECB sets a deposit facility rate alongside its main refinancing operations rate. The BOJ has, for years, operated under a framework that includes negative rates and yield curve control, though that has shifted recently. Different mandates, different tools, different priorities.

What unites them is the decision-making process. Rate-setting committees meet on scheduled dates, review economic data, and vote. Markets watch not only the decision but the accompanying statement, the press conference, and any updated economic projections. A hold can move markets as much as a cut if the language changes.

Traders who follow forex seriously track these meeting calendars the way a sports bettor tracks fixture lists. Missing one is rarely an option.

The mechanism linking rates to exchange rates

Consider a simple scenario. The Fed raises rates by 25 basis points while the ECB holds steady. Suddenly, dollar-denominated bonds offer a higher yield than comparable euro-denominated bonds. A pension fund in Frankfurt looking for safe yield now has a reason to shift allocation toward US Treasuries. To buy those Treasuries, it must convert euros into dollars.

Multiply that decision across thousands of institutional investors, sovereign wealth funds, and corporate treasurers, and the result is sustained demand for dollars and corresponding selling pressure on euros. EUR/USD falls.

This is the basic transmission mechanism, though reality layers on complications. Capital flows respond to expected rates as much as actual ones. They respond to risk perception, political stability, and liquidity conditions. A rate hike in an emerging market economy with capital controls or currency risk can fail to attract inflows even when the yield differential is enormous.

For the major pairs — EUR/USD, USD/JPY, GBP/USD, AUD/USD — the link between rate expectations and price action is consistently visible. Bond yield charts and currency charts often move in close parallel, particularly the two-year and ten-year government bond differentials.

Interest rate differentials and the carry trade

The gap between two countries' interest rates is called the interest rate differential, and it sits at the heart of one of the most persistent strategies in forex: the carry trade.

The mechanics are straightforward. A trader borrows in a low-yielding currency, say the Japanese yen at near-zero rates, and uses the proceeds to buy a higher-yielding currency, perhaps the Australian dollar or the Mexican peso. The trader earns the difference between the two rates as long as the position is held, paid out daily through swap or rollover charges in most retail forex platforms.

When markets are calm and risk appetite is healthy, carry trades can run for months, even years. The yen weakened steadily against higher-yielding currencies through long stretches of the 2000s and 2010s for precisely this reason.

But carry trades unwind violently. When risk sentiment turns — a banking crisis, a geopolitical shock, a sudden policy shift — traders rush to close positions, buying back the funding currency and selling the high-yielder. The yen can rally several percent in a single session under those conditions. The differential giveth, and the differential taketh away.

Real vs. nominal rates and inflation expectations

A 5% nominal interest rate sounds attractive until inflation is running at 7%. The lender, in real terms, is losing purchasing power. This is the difference between nominal rates — the headline number — and real rates, which adjust for inflation.

Forex markets care deeply about real rates, particularly over longer horizons. A country with high nominal rates but even higher inflation rarely sees sustained currency strength. Capital may flow in briefly, chasing yield, then flow out as the real return turns negative.

The 2022–2023 cycle offered a clear demonstration. The Fed raised nominal rates aggressively, but US inflation was also running hot. The dollar's strength during that period tracked the trajectory of real rates more closely than nominal ones. When inflation began cooling while rates stayed high, real yields rose, and the dollar held firm well after the hiking cycle ended.

Inflation expectations matter just as much as current inflation. Markets price in where rates are likely to settle two and three years out, and those expectations are baked into bond yields and, by extension, currency pairs. Watching breakeven inflation rates is part of the job.

Market reactions to rate decisions and forward guidance

Rate decisions themselves are often less explosive than the surrounding communication. Markets price in expected outcomes well in advance using fed funds futures, overnight index swaps, and similar instruments. By the time a decision is announced, the consensus expectation is usually built into the currency.

What moves markets is surprise. A hold when a hike was expected. A dovish statement following a hawkish hike. A press conference where the chair refuses to rule out further tightening when traders had assumed the cycle was done.

Forward guidance — the practice of central banks signalling future policy intentions — has become a primary lever. The ECB's "data-dependent" framing, the Fed's dot plot, the BOJ's careful messaging around yield curve adjustments: all of these shape rate expectations months ahead of any actual decision.

This is why the calendar around major central bank meetings sees elevated volatility even on relatively quiet news weeks. Spreads widen. Liquidity thins around the announcement window. Slippage becomes a real risk for orders placed in the minutes either side of the release.

Practical implications for forex traders

Knowing rates matter is one thing. Trading around them is another.

The first practical step is keeping a central bank calendar visible. Major meetings — Fed, ECB, BOE, BOJ, RBA, BOC, SNB, RBNZ — should be marked weeks in advance. Position sizing in the days leading up to a decision deserves reconsideration, particularly for leveraged retail accounts where a 100-pip move can wipe out margin quickly.

Second, watch the bond market. Two-year yield differentials between two countries often lead currency pair movements. When the US two-year yield rises faster than the German two-year, EUR/USD typically weakens. The relationship is not perfect, but it is consistent enough to be useful as a confirmation tool.

Third, separate the noise from the signal. Not every rate decision will move markets meaningfully. The ones that matter are the ones containing genuine surprise — either in the decision itself or in the guidance attached. Trading every meeting with the same intensity is a fast route to overtrading.

Risk management around these events is not optional. Stops can gap. Liquidity can vanish for seconds at exactly the wrong moment.

Conclusion

The connection between interest rates and currency values is among the most reliable relationships in forex, but reliable does not mean simple. Rates move on expectation, on real returns, on relative differentials, on guidance, on the surprise factor surrounding every announcement. A trader who treats rate decisions as binary events — up or down, buy or sell — misses most of what is actually happening.

The deeper skill lies in reading the entire context. What did the market expect? How are real yields trending? What is the differential telling you about flows? Where are bond yields pointing next?

None of this guarantees a profitable trade. Currencies move on dozens of factors, and rates are only one input, however influential. Geopolitics, commodity prices, risk sentiment, and capital flows all interact with rate expectations in ways that can override the textbook response on any given day.

What rate analysis offers is a framework. A way of organising information that turns the constant flow of central bank headlines into something tradable. For anyone serious about the major pairs, it is the bedrock the rest of the analysis rests on.